Gold hit another new all-time high last week, approaching USD 2700/oz, positioning it as one of the top performing assets so far this year. Likewise precious metals miners are delivering strong performance, relative both to gold and to broader equities. Market conditions for gold are increasingly supportive, backed by strong physical demand, a positive macroeconomic environment and improving investor sentiment. Silver is also benefitting from these drivers, as well as from rising industrial demand forecasts, notably from solar energy. As momentum builds, investors face the question of whether physical bullion or precious metals miners will lead the way as the next phase of the bull market develops.

Bullion and miners share common drivers, yet the returns profile of these two asset classes differ somewhat. Physical gold and silver are real assets, ‘safe haven’ investments, and can be considered an inflation hedge, yet pay no yield. Miners provide operational leverage to gold and silver prices, can pay dividends, offer exploration and discovery upside, yet are susceptible to cost pressure. Typically, precious metal miners outperform physical gold by 2-5x during a bull market and, as in previous upcycles, we consider miners are poised to outperform in the months ahead[i].

Gold miners or gold – Gold miners are poised to outperform gold during the next phase of the bull market, as producers face a re-rating on the back of margin expansion and the return of western investors to the sector.

Capital discipline and dividends – Capital discipline appears to be holding and costs are under control. Gold miners are on a c.2% dividend yield, surpassing that of the S&P500[ii].

Selective M&A – Stronger cash accumulation is allowing miners to engage in selective M&A, typically targeting assets which offer them a competitive advantage. Geopolitical risk remains high for assets in some regions.

What’s next for the precious metals sector? – Gold and silver prices are supported by robust physical demand, a supportive macroeconomic environment, improving investor sentiment and turbulent geopolitics.

Will margin expansion drive a re-rating for precious metals miners?

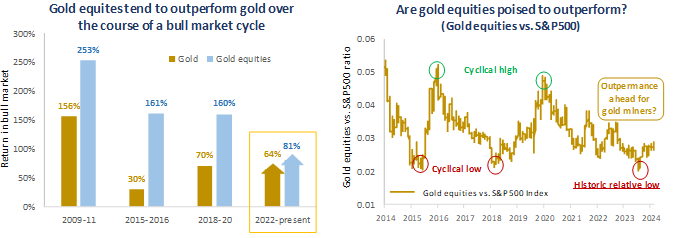

Since the gold sector’s cyclical low in October 2022, gold equities have rallied 81%, exceeding gold’s rise of 64%[iii]. Yet, as illustrated on the chart below, this performance is pedestrian compared to previous upcycles. While gold miners have delivered strong returns over the past two years, history suggests the bull market for gold equities has a lot further to run. The 2018-20 bull market saw gold rise 70% while miners rallied 160%, while the 2015-16 upcycle saw gold gain 30% and miners 161%. Furthermore, relative to US equities, gold equities appear poised for a period of outperformance having turned a corner since hitting historic relative low valuations in late-2023.

Figure 1

Sources: Bloomberg. Baker Steel internal. Data at 25 September 2024.

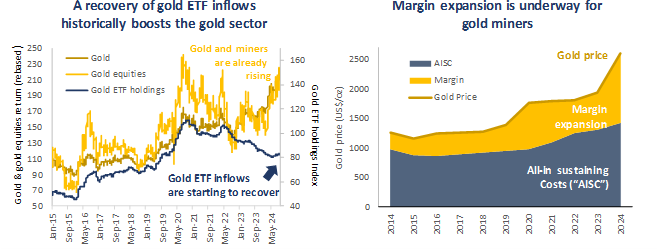

At this point in the cycle, margin expansion and a revival of investor sentiment are key drivers for precious metals equities. Miners’ margins are set to expand in 2024, as precious metals prices rise by more than costs. With the average all-in sustaining cost (“AISC”) of producing an ounce of gold at just over USD 1400/oz, and the gold price today at USD 2600/oz, the sector’s profitability is strong[iv]. Costs are rising, yet the pace of inflation has slowed significantly over the past two years. Certain costs, such as state royalties, are unavoidable yet overall cost control has been managed well, aided by technology and a persistent focus on capital discipline. This improvement in profitability is taking place against a backdrop of a recovery of investor sentiment towards precious metals miners. Flows into both physical gold and gold equity ETFs are picking up, following three years of net outflows. We believe this trend will continue as monetary conditions start to ease, potentially accelerating a rotation away from growth stocks towards value. This is highly significant for the precious metals sector, which remains substantially undervalued relative to broader equity markets.

Figure 2

Sources: Bloomberg, World Gold Council, Metals Focus. Data at 25 September. Note, AISC data as at 31 March 2024.

In previous cycles, the combination of expanding margins for miners and resurgent ETF buying has driven gold higher and boosted precious metals miners. With these factors in place, the stage is set for gold equities to deliver substantial outperformance of physical gold in the next phase of the bull market, in an environment we believe will be ripe for stock pickers to thrive.

How can precious metals miners enhance portfolio returns?

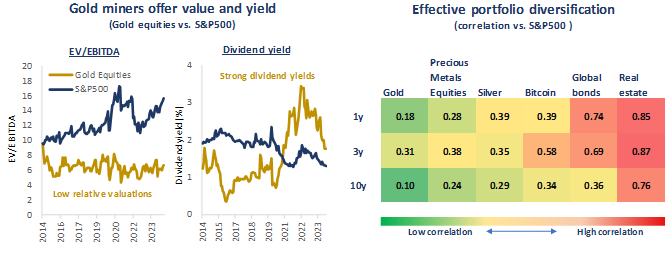

Precious metals equities offer several key portfolio benefits. Firstly, miners’ low relative valuations and potential for near-term re-rating, as discussed above, make the sector a compelling value proposition. Secondly, dividend yields have been strong in recent years, alongside buybacks, and appear likely to remain higher than general equity markets (as illustrated on the chart below), reflecting miners’ strong margins.

Figure 3

Source: Bloomberg. Data at 25 September 2024.

Thirdly, gold and precious metals equities offer true diversification. As illustrated on the table above, the sector has a very low correlation to the S&P500, just 0.1 for gold and 0.24 for miners over ten years[v]. This compares to other sectors, notably real estate and cryptocurrencies, which are sometimes considered to be portfolio diversifiers but in reality have a significantly higher correlation to the US stock market compared to the precious metals sector[vi].

At company level, we consider that miners are in strong financial and operational shape. Baker Steel’s team has recently returned from the Denver Gold Forum Americas and several mining company site visits which, combined with Q2 results, reinforced our view that the sector is poised for re-rating. Alongside offering compelling value and shareholder returns, the sector is seeing selective M&A deals. Recent deals highlight positive trends as producers are seeking assets which build on their competitive advantage, for instance assets in familiar jurisdictions rather than far-flung locations. However, quality assets with low cost profiles are rare, and geopolitical risk remains a key concern. Regarding exploration and development, we see that exploration budgets are clearly increasing. Yet while there have been some excellent recent discoveries, these require years of permitting and funding. Most of the large capital projects have already been undertaken by the companies, and we see few excellent projects on the horizon.

What’s next for the precious metals sector?

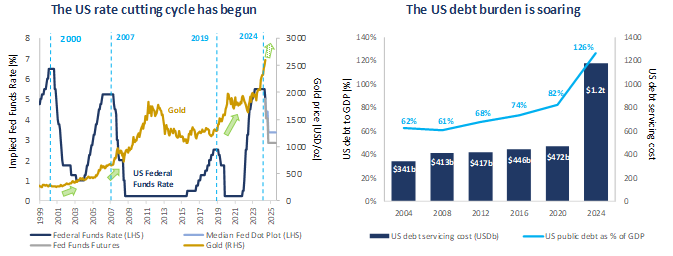

With upcoming US elections, monetary policy easing and heightened economic and political risk globally, momentum in the precious metals sector appears set to continue. From emerging market central banks to retail investors in the US and Asia, demand for physical gold remains strong. With western institutions starting to return to the sector we expect to see demand growth continue in the months ahead. The US presidential election will be a dominant theme across markets for the fourth quarter of 2024. The Trump vs. Harris contest holds significant implications for the natural resources sector, specifically relating to the outlook for trade wars and the green energy transition in the US. A Trump victory would raise uncertainty over the future of the Inflation Reduction Act, yet with many beneficiaries of this policy located in red states, the changes may be less than feared. For the precious metals sector, we consider that the major drivers for gold and silver are largely insulated from the elections outcome. Neither candidate favours a significant reduction in spending or debt expansion, indicating the long-term trend towards debasement of the US dollar will likely continue. US debt servicing has now exceeded USD 1.2 trillion annually, with no credible plan to reduce this burden[vii]. Meanwhile, many emerging market central banks, notably the BRICS, are actively diversifying away from US Treasuries, while simultaneously increasing their gold reserves.

Figure 4

Sources: Bloomberg. Data at 25 September 2024.

Importantly, the major macroeconomic catalyst for gold, the interest rate cutting cycle, has commenced with the world’s two largest economies, the US and China, both now cutting rates. The Fed’s pivot in September towards potentially larger cuts highlighted that they now see unemployment, rather than inflation, as their top priority. This is significant for the precious metals sector, as periods of falling US interest rates have historically been highly positive for gold and precious metals miners. The gold sector’s positive reaction to the start of monetary policy easing appears similar to previous cycles, suggesting the bull market, particularly for miners, has a way to go.

Against this supportive macroeconomic backdrop, we consider that precious metals miners have rarely been so well-positioned for outperformance. Precious metals equities are a sector where actively managed portfolios have historically tended to outperform, certainly during bull markets. Given the disparities in quality between assets, ESG issues and technical factors we consider that bottom-up company research and fundamental analysis is the most effective investment approach to unlock value for investors. Alongside this, top-down asset allocation analysis can add value and ensure the appropriate mix of sub-sectors, geographic exposure, market capitalisation and company status to deliver superior risk adjusted returns. As in previous cycles, an investment in precious metals miners can generate substantial returns for investors, with active management significantly enhancing these returns.

Baker Steel Capital Managers LLP manages three award winning investment strategies, covering precious metals equities, speciality metals equities and diversified mining.

Baker Steel has a strong track record of outperformance relative to its peers and relative to passive investments in the metals and mining sector. Fund Managers Mark Burridge and David Baker have been awarded two Sauren Gold Medals for 2022 and were awarded Fund Manager of the Year at the 2019 Mines & Money Awards.

Baker Steel’s precious metals equities strategy is a 2023 winner for the sixth year running of the Lipper Fund Awards while Baker Steel Resources Trust has been named Investment Company of the Year 2021, 2020, 2019, Natural Resources, by Investment Week.

Sources: S&P, USGS, Benchmark Mineral Intelligence, Albemarle, Bloomberg, Bloomberg New Energy Finance.

Important

Please Note: This document is a financial promotion is issued by Baker Steel Capital Managers LLP (a limited liability partnership registered in England, No. OC301191 and authorised and regulated by the Financial Conduct Authority) for the information of a limited number of institutional investors (as defined in the Fund prospectus) on a confidential basis solely for the use of the person to whom it has been addressed. This document does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or purchase any shares or any other interests nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefor. Recipients of this document who intend to apply for shares or interests in Baker Steel’s funds are reminded that any such application may be made solely on the basis of the information and opinions contained in the relevant prospectus or other offering document relating thereto, which may be different from the information and opinions contained in this document. This report may not be reproduced or provided to any other person and any other person should not rely upon the contents. The distribution of this information does not constitute or form part of any offer to participate in any investment. This report does not purport to give investment advice in any way. Past performance should not be relied upon as an indication of future performance. Future performance may be materially worse than past performance and may cause substantial or total loss.