Gold above $3,100/oz, but are miners just getting started?

Amid gold’s historic breakout, precious metals miners appear to be in the foothills of a new bull market

Gold has surpassed USD 3,100/oz for the first time, continuing its historic bull market following a period of healthy consolidation in late-2024. As the “Trump trades” have faded, investors’ focus is shifting to the risks facing US growth and rising economic uncertainty. Global financial markets are in a period of flux, as Trump’s tariffs, coupled with tense geopolitics and growing economic imbalances, prompt investors to seek diversification and value. The resilience of gold’s bull market highlights the deep pool of buyers globally, from central banks and institutional investors to high-net-worth and retail buyers. The broad appeal of gold creates a situation where at least one of these groups of investors is typically looking to add to their gold position. Pullbacks will continue to occur, yet these have proven shorter and shallower than many investors expected.

As investor sentiment towards gold becomes increasingly bullish, precious metals miners appear poised for outperformance. Margin expansion is underway for miners as the gold price moves higher and costs remain largely under control. Balance sheets are strong, and buybacks are increasing. Precious metal miners are trading at severely depressed levels relative to broader equity markets, yet a turning point appears to have arrived as investors begin to return to the gold sector. Given the relatively small size of the gold mining sector, even a minor rotation into these undervalued equities is likely to drive a significant rise in share prices.

As gold exceeds USD 3,100/oz, we identify some key themes for precious metals miners –

- Precious metals are supported by strong fundamentals – Central bank buying and physical demand is strong, while a resurgence of ETF buying indicates investor sentiment is recovering.

- Macroeconomic conditions indicate further strength – Sticky inflation, pressure on the US dollar, and rising risks to the US financial position and equity markets create a supportive environment for gold.

- Miners appear to have a lot further to run – Gold miners typically deliver 2-5x leverage to rising gold prices in a bull market, yet miners remain well below recent The upside potential is substantial.

- A range of other speciality and industrial metals appear poised for outperformance – Copper miners and silver miners in particular face a strong outlook, amid rising physical prices and strong balance sheets.

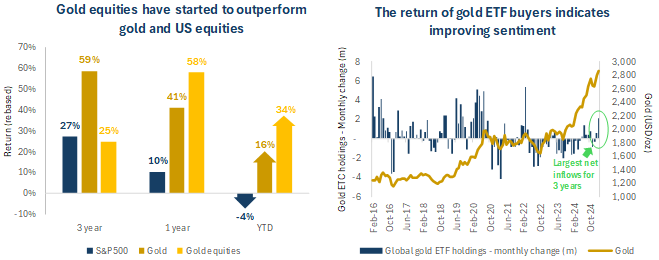

Figure 1

Source: Bloomberg. Data at 18 March 2025.

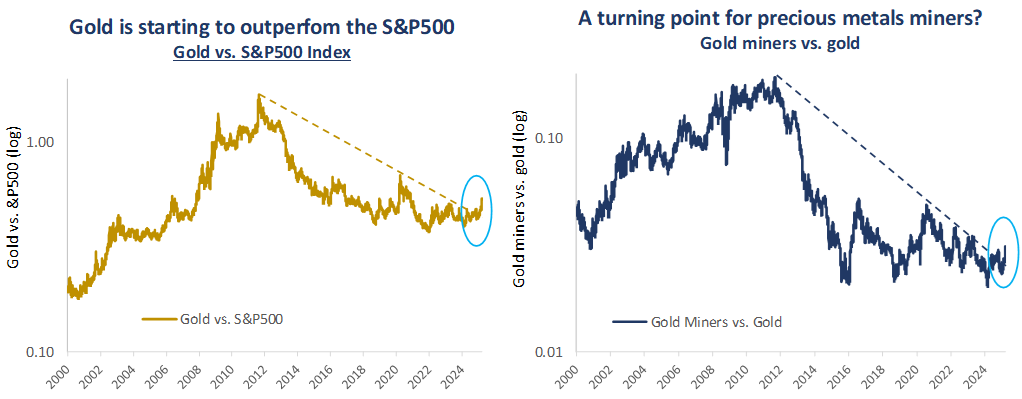

The strength and speed of gold’s bull market has taken many market observers by surprise, and its core drivers suggest that the market is well supported at these levels. Recent new highs have been driven by strong physical demand for gold from a range of investors. From central banks increasing gold reserves, to institutions seeking diversification to individual investors looking for a safe haven, gold’s relevance continues to grow under current macroeconomic conditions. Gold ETFs saw the biggest monthly inflows in three years in February, signalling a bullish shift in investor sentiment towards the gold sector. Gold has been outperforming the S&P500 over the past year, while miners have also started to outperform physical gold. We believe a turning point has been reached and the capital rotation underway will continue to cause precious metals miners to deliver leverage to the gold price as it continues to move higher.

Figure 2

Source: Bloomberg. Data 20 March 2025.

The gold price’s c.USD 1,000/oz appreciation over the past year is transformative for miners’ profitability. Precious metals miners have performed well as gold prices have risen, yet we believe there is substantial potential for re-rating as company results continue to indicate that cost control and capital discipline are holding, and margins are expanding. Previous gold bull market cycles have seen miners deliver 2-5x leverage to rising gold prices[i]; a relationship we believe could be restored as sentiment starts to return to the sector.

A macroeconomic sea change indicates strength ahead for precious metals

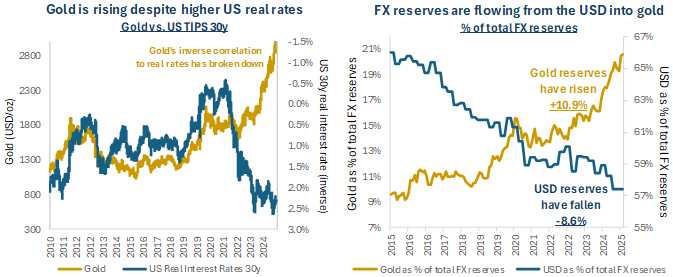

We consider that the strong demand trends mentioned above reflect a fundamental shift underway in macroeconomic conditions for gold. Historically the gold price has been heavily influenced by a combination of US interest rates, inflation expectations and the US dollar. Yet the past three years have seen a breakdown of these relations, particularly gold’s typically inverse correlation to US real interest rates (as shown on the chart below).

The disconnect of the gold price from its historic drivers reflects a shift in the fundamental buyers which are currently driving demand for gold. Central banks’ gold demand continues to underpin the market, with annual purchases exceeding 1,000 tonnes for the past three years[ii]. Poland and Turkey were among the largest buyers during 2024 alongside the PBOC. Other fundamental buyers of gold include a range of institutional and retail investors around the world, boosted by safe haven buying in the face of global economic uncertainty. News that China’s insurance companies may be able to, and may be encouraged to, hold gold is also a potentially substantial demand driver. These investors appear less influenced by US interest rates and the outlook for the US dollar than western institutional investors who, as mentioned above, have been largely absent from the market in recent years but are showing sings of returning, as evidenced by rising gold ETF inflows[iii].

Figure 3

Source: Bloomberg. Data at 28 February 2025.

Underlying this shift is a sea change in the role of gold and other hard assets for investors and policymakers, relative to the US dollar and US assets. Firstly, de-dollarization is underway as countries, most notably amongst the BRICS economies, with China having reduced its US treasury holdings by 38% over the past decade[iv]. The cancellation of Russia’s US treasury holdings in the aftermath of the invasion of Ukraine accelerated this trend. Meanwhile many countries continue to accumulate gold reserves. As shown on the chart above, US dollar reserves have declined -8.6% as a percentage of total FX reserves over the past decade, while the proportion of gold has risen by 10.9%[v]. Secondly, the US itself faces risks to its financial position, which appears likely to drive safe haven demand for gold. The US dollar has been trending lower since Trump’s inauguration, amid renewed concerns over slowing growth and potentially stagflation, amid persistent inflation. While the prospect of further US rate cuts has weakened, in our view hikes still appear unlikely. Meanwhile the deficit is expected to continue to expand. The US spending bill passed in early March delivered USD 4.5 trillion tax cuts and just USD 2 trillion of spending cuts, leaving federal government debt USD 2.5 trillion higher[vi]. Despite the efforts of the new Department of Government Efficiency, known as DOGE, US debt continues to rise, pushing the debt burden to over USD 1 trillion in 2025[vii], leaving the risk skewed to the upside for gold.

Speculation has arisen regarding a potential revaluation of US gold stockpiles, which have been officially valued at USD 42/oz ounce since 1973. A revaluation to current prices would see US gold reserves jump from around USD 11 billion to over USD 800 billion[viii]. While offering a potential route to strengthening the US balance sheet, even this would ultimately be a drop in the ocean of debt, paying for not even one year’s interest. However, from our view the fact that this option is even being discussed, highlights gold’s growing importance as a financial asset and geopolitical tool. Elsewhere, the physical gold market has been in the spotlight in recent months, as speculation abounds over physical shortages of gold on certain exchanges. The rush to repatriate gold to the US in recent months has caused turmoil in physical markets, most visible at the Bank of England where waiting times for withdrawals surged to up to eight weeks during February. Amid these delays we note that COMEX is distancing itself from LBMA, via the removal of certain OTC contracts, at a time with some market participants questioning the ability of LBMA to deliver physical gold[ix]. Overall, it is reported that since December 2024, over 600 tons of gold have been moved into the vaults of New York[x].

Are precious metals miners in the foothills of a new bull market?

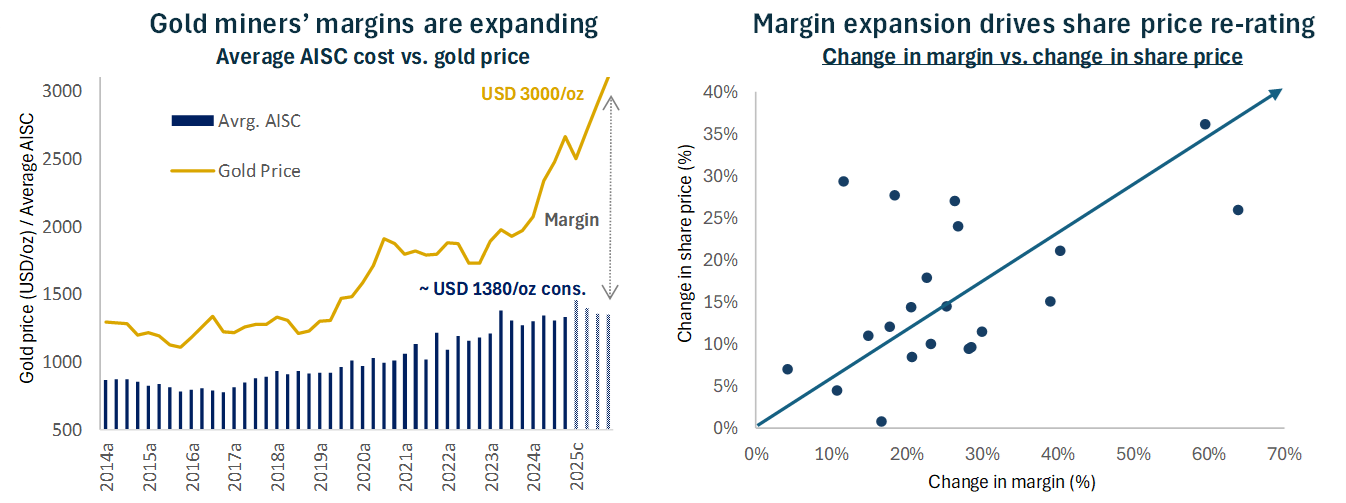

Gold’s recent gains present a transformative opportunity for precious metals miners, many of which face a profitability boost likely to drive an increase in investor sentiment towards this often-overlooked sector. Recent years have seen precious metals equities face extreme undervaluation, with gold miners’ P/NAVs having declined 46% from 2020 highs[xi] and with gold equities trading at just 5.0x EV/EBITDA, compared to 18.9x multiples for technology equities[xii]. This undervaluation is particularly stark given the fundamentals are increasingly strong for precious metals miners. Q4’24 results have been encouraging, with many companies demonstrating production growth and cost control. With average all-in sustaining costs (“AISC”) at around USD 1380/oz miners receive a substantial margin, as shown on the chart below, while conservative ore reserve planning is showing good discipline. We see a clear positive correlation between a mining company’s margin expansion and its share price re-rating, as shown on the chart below.

Figure 4

Source: Baker Steel internal estimates, Visible Alpha, Bloomberg, Company Reports. Note: AISC cover large-cap gold miners (>1moz).

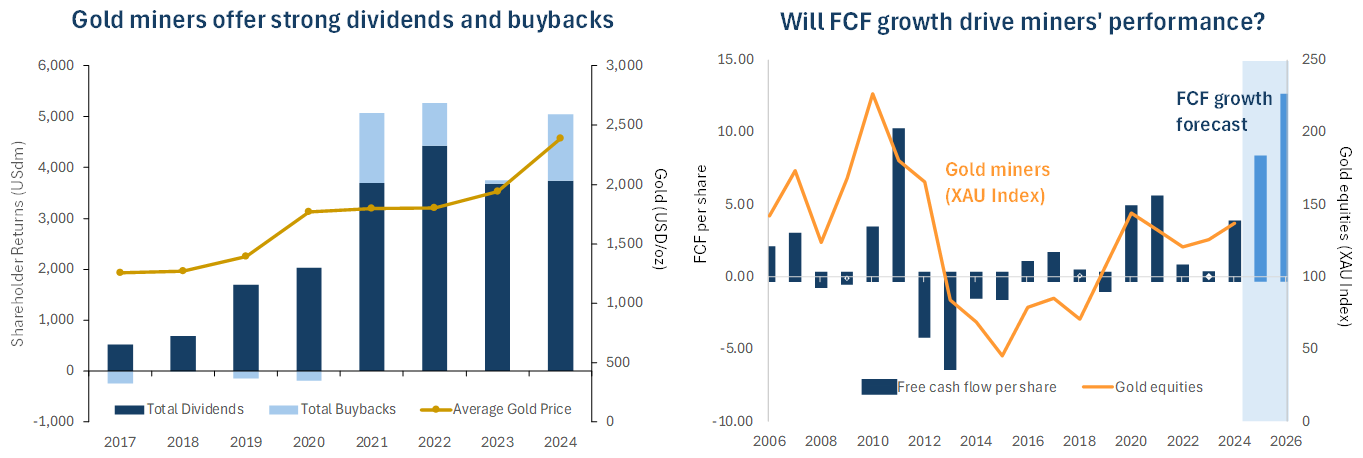

In terms of performance, the upside potential for precious metals miners is significant, as miners have yet to deliver the scale of performance seen in previous gold cycles. Historically, miners have delivered a 2-5x leverage during gold price rallies, yet during the current cycle, performance has been largely in line with the physical metal.

We see two reasons for gold equities’ valuation lag. Firstly, concerns over sustainability of the gold price and the costs and capital discipline in the sector, and secondly a lack of interest from western investors in the metals sector due to a focus on mainstream equities. Notably, despite recent inflows into physical gold ETFs, major gold equity ETFs have yet to see any marked pickup in inflows signalling investors are yet to begin allocating meaningfully to this sector[xiii].

Yet we believe gold miners appears increasingly attractive to investors. Alongside low valuations, as margins expand, we are also seeing gold miners returning more capital to shareholders, supported by strong gold prices and robust free cash flow. Dividends are rising in line with existing policies, though some companies are beginning to revise payout frameworks for greater flexibility. Share buybacks are becoming a more popular way to return excess cash, for example Newmont Mining expanded its program to USD 3 billion, Barrick Gold increasing to USD 1 billion, and Kinross Gold and B2 Gold are looking at reinstating buybacks[xiv].

Figure 5

Source: Bloomberg, Company Reports, Baker Steel internal. Data at 31 December 2024. Estimated FCF data for 2025 and 2026.

The sector’s health is also reflected in the recent M&A activity amongst gold companies, where it is often cheaper to buy than to build at present. March saw Ramelius Resources agree to take over Spartan Resources for AUD 2.4 billion, while Gold Road Resources rejected a USD 2.1 billion bid from Gold Fields[xv]. Between buybacks and more external buyers, the outlook for precious metals miners appears strong. Furthermore, it appears that discipline is holding in this cycle so far. Gold price assumptions for ore reserves have risen just 17% over five years to 2024 (i.e. no real increase), while gold prices have risen 71% over the period. This compares to the 2007-2012 cycle, when gold price assumptions soared by 161%, while gold prices rose 141%[xvi]. In general terms there has been no change, on a mine by mine basis, to the cutoff grade being utilized within reserve assumptions. With regards to production and cost guidance and expectations, gold miners generally hit or exceeded guidance in 2024. Cost control was broadly in place and appears under control for 2025. Production growth has been largely flat over the past year, indicting that production is not being recklessly increased, and amid conservative production guidance.

What other metals are poised for medium to long-term outperform?

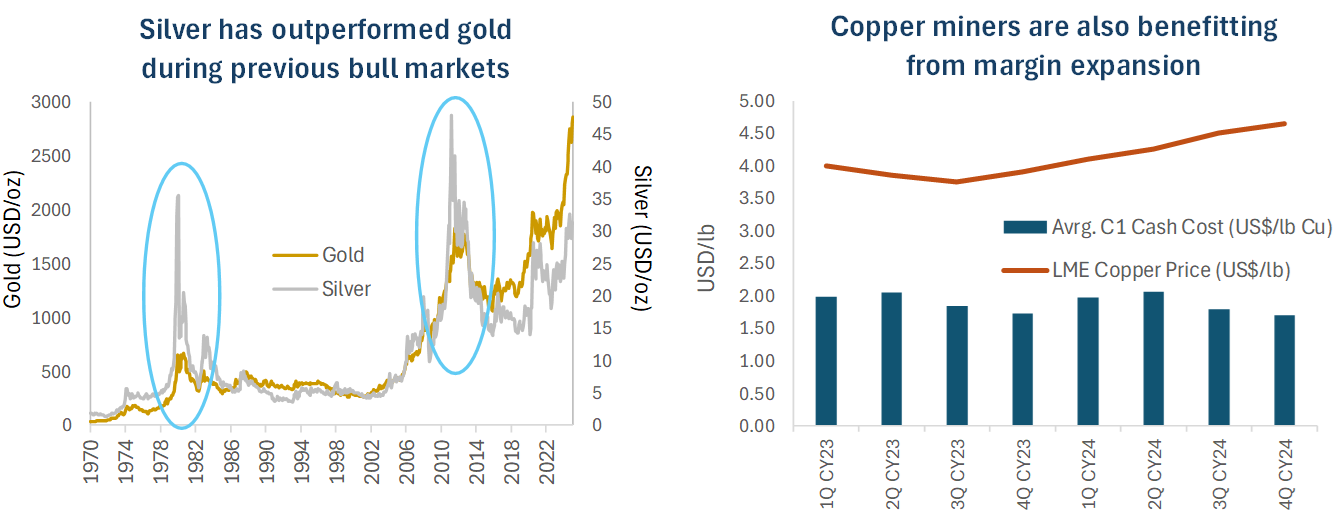

Alongside rising demand for gold, we see opportunities across a range of metals at present. While short-term volatility may continue, due to industrial factors, copper and silver miners are particularly well-positioned for medium-term outperformance. Beginning with silver, the metal has lagged gold for some time yet continues to exhibit high beta to movements in the gold price. The silver market has been in a structural deficit since 2021, estimated to be 149moz in 2025[xvii]. Investment demand has been weak in recent years, with silver facing a lack of western investor interest in a similar manner to gold. The difference for silver is that industrial usage accounts for over 50% of demand and is growing rapidly. Rising demand from solar energy and electronics represents a significant driver for the silver price and for silver miners. By 2030 it is forecast that demand for silver from solar panel production alone will account for around 29% of annual silver supply, compared to around 23% in 2024[xviii]. In our view the importance of silver in technology is often overlooked and we consider silver to be the “unsung hero” of the new industrial revolution.

Figure 6

Source: Bloomberg, Company Reports, Baker Steel internal. Data at 28 January 2025.

Copper miners face a strong outlook at present, as copper prices hit new highs. Copper miners have likewise demonstrated encouraging recent performance, having gained +10% year-to-date[xix], yet we believe the sector has further upside potential. In a similar manner to precious metals producers, copper miners are also capitalising on rising copper prices at a time when costs are largely under control, as highlighted on the chart above. Some copper companies are supported by precious metals by-product credits, giving the sector an additional advantage. Copper production growth remains slow, given copper prices have remained below incentive pricing for new projects for some time.

With the precious metals sector in strong shape and a promising outlook for the other sub-sectors of the metals and mining industry, we believe now is a very interesting time for investors in mining equities. Alongside the recent strength seen in some areas, notably precious metals, we also consider that rising geopolitical concerns over supply chains for critical raw minerals will continue to offer new opportunities to an active investment manager such as Baker Steel. Amid signs of improving investor sentiment, we note that it would only take a small rotation from mainstream equities into mining equities to generate transformative flows, given the small size of the mining equity universe. As we have seen in previous cycles, the sector can generate substantial returns during a bull market, with active management typically enhancing those returns.

[i] Bloomberg, Baker Steel Capital Managers LLP.

[ii] World Gold Council.

[iii] Bloomberg.

[iv] Bloomberg. Data at 28 February 2025.

[v] Bloomberg. Data at 28 February 2025.

[vi] FT.

[vii] Bloomberg.

[viii] World Gold Council, Baker Steel.

[ix] Bloomberg, data at 26 March 2025.

[x] CME Group.

[xi] CNBC, World Gold Council.

[xii] Bloomberg, Canaccord.

[xiii] Bloomberg, data at 28 February 2025.

[xiv] Bloomberg, Market Vectors Junior Gold Miners Index

[xv] Bloomberg, Company Reports, Baker Steel internal.

[xvi] Company Reports, Bloomberg.

[xvii] Bloomberg, Company Reports, Baker Steel internal.

[xviii] Silver Institute.

[xix] IEA, Energy Institute, The Economist, BNEF, Baker Steel internal forecasts.

About Baker Steel Capital Managers LLP

Baker Steel Capital Managers LLP manages three award winning investment strategies, covering precious metals equities, speciality metals equities and diversified mining.

Baker Steel has a strong track record of outperformance relative to its peers and relative to passive investments in the metals and mining sector. Fund Managers Mark Burridge and David Baker have been awarded two Sauren Gold Medals for 2022 and were awarded Fund Manager of the Year at the 2019 Mines & Money Awards.

Baker Steel’s precious metals equities strategy is a 2023 winner for the sixth year running of the Lipper Fund Awards while Baker Steel Resources Trust has been named Investment Company of the Year 2021, 2020, 2019, Natural Resources, by Investment Week.

Sources: S&P, USGS, Benchmark Mineral Intelligence, Albemarle, Bloomberg, Bloomberg New Energy Finance.

Important

Please Note: This document is a financial promotion is issued by Baker Steel Capital Managers LLP (a limited liability partnership registered in England, No. OC301191 and authorised and regulated by the Financial Conduct Authority) for the information of a limited number of institutional investors (as defined in the Fund prospectus) on a confidential basis solely for the use of the person to whom it has been addressed. This document does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or purchase any shares or any other interests nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefor. Recipients of this document who intend to apply for shares or interests in Baker Steel’s funds are reminded that any such application may be made solely on the basis of the information and opinions contained in the relevant prospectus or other offering document relating thereto, which may be different from the information and opinions contained in this document. This report may not be reproduced or provided to any other person and any other person should not rely upon the contents. The distribution of this information does not constitute or form part of any offer to participate in any investment. This report does not purport to give investment advice in any way. Past performance should not be relied upon as an indication of future performance. Future performance may be materially worse than past performance and may cause substantial or total loss.